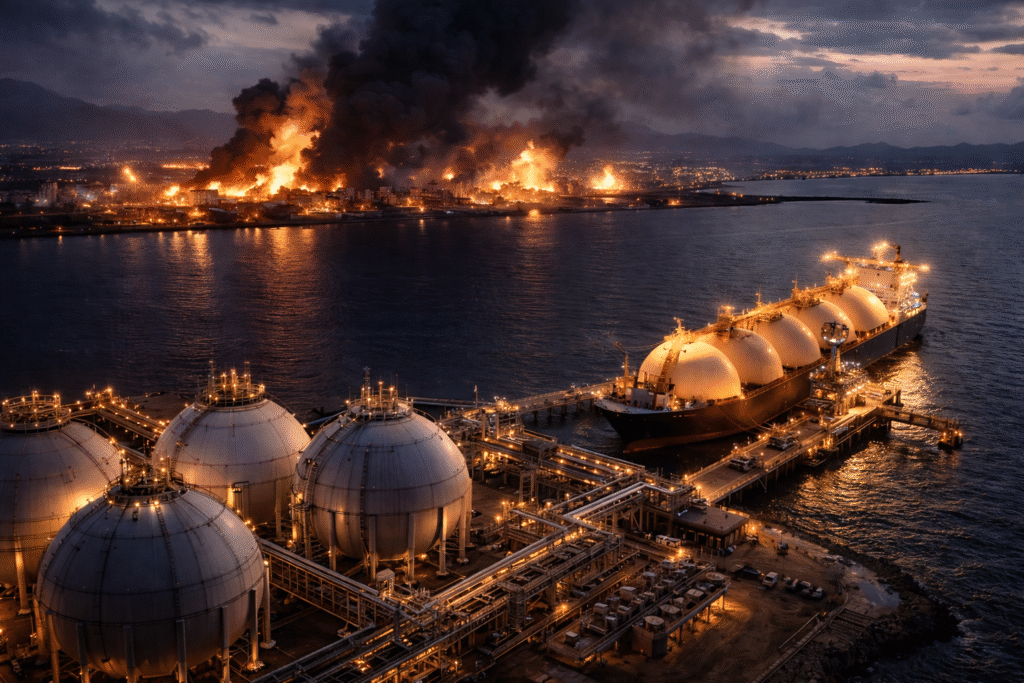

LNG Flows at Risk

Global natural gas markets jolted higher this week as escalating conflict in the Middle East raised fears of supply disruption through the Strait of Hormuz — a critical artery for global energy trade.

The narrow waterway between Oman and Iran handles roughly one-fifth of global LNG shipments, making it a key pressure point for Europe and Asia.

European benchmark Dutch TTF futures surged as much as 35% in a single session, climbing above €60 per megawatt-hour and posting weekly gains approaching 76%.

Asia’s Japan-Korea Marker (JKM) also jumped to a one-year high.

Qatar Production Halt Raises Alarm

Qatar, one of the world’s largest LNG exporters, temporarily halted production following drone strikes on key industrial sites. Estimates suggest the pause could reduce near-term global LNG supply by nearly 19%.

Reports of Iranian forces closing the Strait of Hormuz to ship traffic added to the anxiety, though U.S. officials indicated the route remained operational.

Even a short disruption could significantly tighten global gas balances.

Europe Faces the Greatest Risk

Europe remains highly exposed to LNG shocks. Roughly a quarter of its gas supply comes from LNG imports.

Analysts warn that if flows through Hormuz are restricted for an extended period, the situation could resemble the 2022 energy crisis triggered by supply cuts from Russia.

During that crisis, European gas prices soared to extreme levels, driving inflation higher and pressuring economic growth.

Some forecasts now suggest gas prices could climb materially higher if disruptions last weeks rather than days.

Growth Shock Concerns

Higher energy prices carry direct economic consequences.

Sustained increases in natural gas prices:

- Raise industrial input costs

- Pressure household energy bills

- Weigh on fiscal budgets

- Slow economic momentum

Energy importers across Europe and parts of Asia are especially vulnerable.

In contrast, countries with strong domestic production — including Norway and the United States — are less exposed and could even benefit from higher export pricing.

Asia Also in the Crosshairs

Asia is not insulated from LNG volatility.

Several major economies rely heavily on Middle Eastern gas imports, meaning prolonged disruption could strain trade balances and fiscal conditions.

For energy-import dependent economies with limited policy flexibility, the risk of stagflation rises if prices remain elevated.

U.S. Impact More Contained

The United States, supported by domestic shale production and LNG export capacity, faces comparatively limited price risk.

While global prices influence sentiment, domestic supply buffers help moderate the impact on U.S. consumers relative to Europe or Asia.

WSA Take

Energy markets are once again the pressure valve of geopolitics.

Natural gas — not just oil — has become a central vulnerability in global growth models.

If disruptions remain temporary, markets may stabilize. But a prolonged supply squeeze would amplify inflation risks, strain fiscal budgets, and potentially slow economic growth across energy-importing regions.

The 2022 playbook remains fresh in investors’ minds.

And this time, LNG is the flashpoint.

Explore More Stories in Commodities

Disclaimer

WallStAccess is a financial media platform providing market commentary and analysis for informational and educational purposes only. This content does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Readers should conduct their own research or consult a licensed financial professional before making investment decisions.