The rare earth supply chain is still being built in pieces

The US is putting billions of dollars behind a domestic rare earths industry, but much of the material is still moving to Asia.

According to a Financial Times report, rare earth products from MP Materials, Energy Fuels and Phoenix Tailings are being sold to customers in Japan and South Korea, where magnet manufacturing is already far more established.

That is the gap in Washington’s critical minerals strategy.

The US is moving faster on mining, processing and government-backed financing. It has not yet built enough domestic magnet manufacturing to absorb all of the material coming from supported producers.

For now, the supply chain is not fully domestic. It is allied, fragmented and still dependent on downstream capacity outside the US.

Japan and South Korea are ready buyers

The immediate demand is coming from countries that already have the industrial base to turn rare earth materials into usable components.

Japan remains the largest producer of rare earth magnets outside China. South Korea also has a more developed downstream manufacturing base than the US.

That makes both countries natural buyers for American-backed supply.

Phoenix Tailings CEO Nick Myers told the Financial Times that the company’s customers are “primarily in Korea and Japan,” where demand has surged after China tightened export restrictions.

His warning was direct: “Unless the [US defence] primes move quickly, I will sell out.”

The message is clear. US-backed producers cannot wait indefinitely for domestic buyers to appear when Asian customers are already paying for supply.

China’s export controls are changing the market

The shift comes as China tightens exports of rare earths and other critical minerals.

That has pushed the US and its allies to accelerate efforts to secure alternative supply chains for materials used in defense systems, electric vehicles, wind turbines, electronics and advanced manufacturing.

Rare earth magnets are especially important.

Neodymium-iron-boron magnets, known as NdFeB magnets, are among the strongest permanent magnets available. They are critical in electric motors, drones, missiles, robotics, industrial machinery and other high-performance systems.

China still dominates that market.

According to US government estimates cited in the report, China accounts for about 90% of global NdFeB magnet production. That level of control is why Western governments are trying to build alternatives.

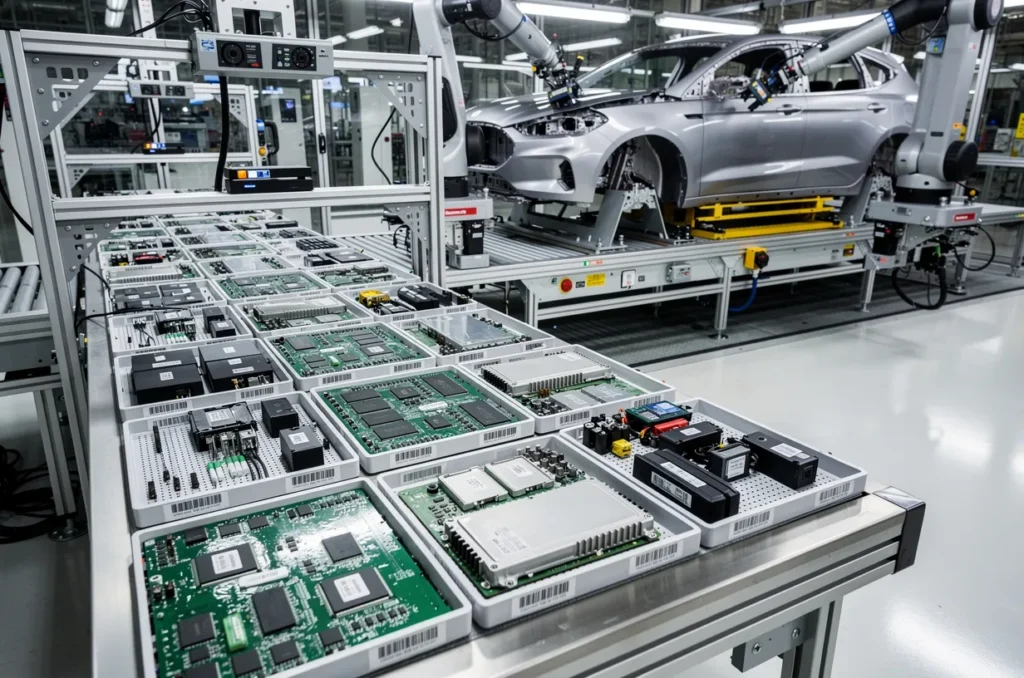

But replacing China’s role requires more than mining rare earth ore.

It requires refining, separation, metal-making, alloy production, magnet manufacturing and customer qualification. Each stage takes time, capital and technical expertise.

MP Materials is shifting away from China

MP Materials remains the largest US rare earth producer and owns the Mountain Pass mine in California.

The company said sales of its neodymium-praseodymium oxide and metal were primarily made through Sumitomo Corp. for distribution to Japanese customers, according to its latest quarterly results.

That is a meaningful change in direction.

MP has stopped selling mined rare earths to China’s Shenghe Resources under its agreement with the US government. Instead, the company is trying to move further downstream and build a more integrated US supply chain.

The next step is magnets.

MP expects to begin shipping finished magnets to General Motors later this year under previously announced supply agreements with GM and Apple.

That would be an important milestone because it moves the company closer to the finished-product stage of the supply chain, where strategic value is highest.

Energy Fuels is building through acquisitions

Energy Fuels is also moving deeper into rare earths.

The company received conditional US government funding worth $725 million last month and expects to export material to Asia in the near term.

Energy Fuels has said it plans to ship rare earth oxides to South Korea while advancing its acquisition of Australian Strategic Materials, whose South Korean facility produces rare earth metals.

The company also agreed in June to acquire German magnet maker Vacuumschmelze in a $1.9 billion deal.

That acquisition is expected to increase shipments to the company’s US operations and give Energy Fuels a stronger position across the rare earth magnet chain.

The strategy reflects the industry’s main challenge. Companies are not only trying to produce material. They are trying to assemble the missing industrial steps around it.

Phoenix Tailings shows the demand problem

Phoenix Tailings has secured conditional government support of $500 million to expand production of rare earth metals and oxides.

That funding is designed to help build domestic capacity.

But the company’s commercial reality shows why the market is moving faster than US procurement.

If American defense contractors and industrial buyers do not move quickly enough, rare earth producers will sell into markets where demand is already established. Japan and South Korea are willing buyers because they have the factories, customers and magnet supply chains already in place.

That does not mean the US strategy is failing.

It means the upstream side is developing faster than the downstream side.

Until US magnet manufacturing expands, rare earth producers will remain partly dependent on allied Asian markets to generate revenue and keep projects moving.

Government support is buying time

The US government is trying to bridge the gap with funding, pricing support and strategic agreements.

MP Materials continues to benefit from a federal pricing agreement that guarantees minimum prices for certain products while the broader supply chain develops.

Energy Fuels and Phoenix Tailings have also secured conditional support tied to rare earth production and processing.

Those policies matter because rare earth supply chains are difficult to build on normal market terms.

China’s existing scale gives it cost advantages. Western producers face higher capital costs, longer permitting timelines and the need to qualify products with demanding industrial and defense customers.

Government support can help offset those barriers.

But it cannot instantly create a full domestic magnet industry.

The bottleneck has moved downstream

The rare earth problem is no longer only about mine supply.

The US is beginning to solve parts of the upstream challenge through MP Materials, Energy Fuels, Phoenix Tailings and other supported projects. The more difficult issue is now downstream manufacturing.

Magnets are where rare earths become strategically useful.

Without enough domestic magnet capacity, US-backed materials may still leave the country before returning in finished components, if they return at all.

That creates a strategic mismatch.

The US wants domestic control over critical minerals. Producers need customers now. Asian allies have the manufacturing base. China still dominates the largest part of the market.

This is how supply chains transition in the real world: unevenly, with bottlenecks shifting from one stage to the next.

WSA Take

The Financial Times report highlights the central challenge in America’s rare earth strategy.

The US can fund mines, processors and metal producers, but the value of rare earths is ultimately captured in the products they enable. For defense systems, electric vehicles and advanced manufacturing, that means magnets.

Right now, Japan and South Korea are better positioned to absorb US-backed supply because they have more developed downstream capacity.

That makes the current system less domestic than policymakers want, but still strategically useful. Selling to allied markets is better than relying on China. It keeps non-Chinese supply chains alive while the US works to build magnet capacity at home.

The risk is timing.

If US defense primes, automakers and industrial buyers move too slowly, producers will lock in commercial relationships overseas. Once those channels are established, domestic buyers may have to compete harder for supply later.

The rare earth trade is entering its second phase.

The first phase was about proving non-Chinese supply could be financed. The next phase is about whether the US can build enough downstream manufacturing to keep that supply inside its own industrial base.

Explore More Stories in Commodities

Disclaimer

WallStAccess is a financial media platform providing market commentary and analysis for informational and educational purposes only. This content does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Readers should conduct their own research or consult a licensed financial professional before making investment decisions.